Evolution AB: Europe’s Most Mispriced Cash Machine

The House That Always Wins — and no one talks about IT

Overview

I. What Is Evolution Gaming?

II. Business Model

III. Valuation

IV. Hidden Gem

V. I Am Buying

I. What is Evolution Gaming?

Evolution Gaming AB is a Swedish company that dominates the global live casino B2B market, offering streamed dealer games to online casinos. They don’t run the casinos — they sell the tools to the top players. Yet the stock is being slept on, and is the biggest steal this decade this very moment.

II. Business Model

So, why is Evolution special?

Evolution creates, produces, markets, and licenses comprehensive online casino solutions tailored for business-to-business gaming operators. While their expertise lies in live casino games such as roulette, blackjack, baccarat, and poker — streamed from proprietary studios with real human dealers. What makes Evolution the undisputed “King” is their exclusive live game shows — titles like Crazy Time, Monopoly Live, and Lightning Roulette — which blend RNG mechanics, flashy studio design, and audience engagement. These shows have become cultural assets within online gambling, commanding player loyalty and creating serious stickiness for operators.

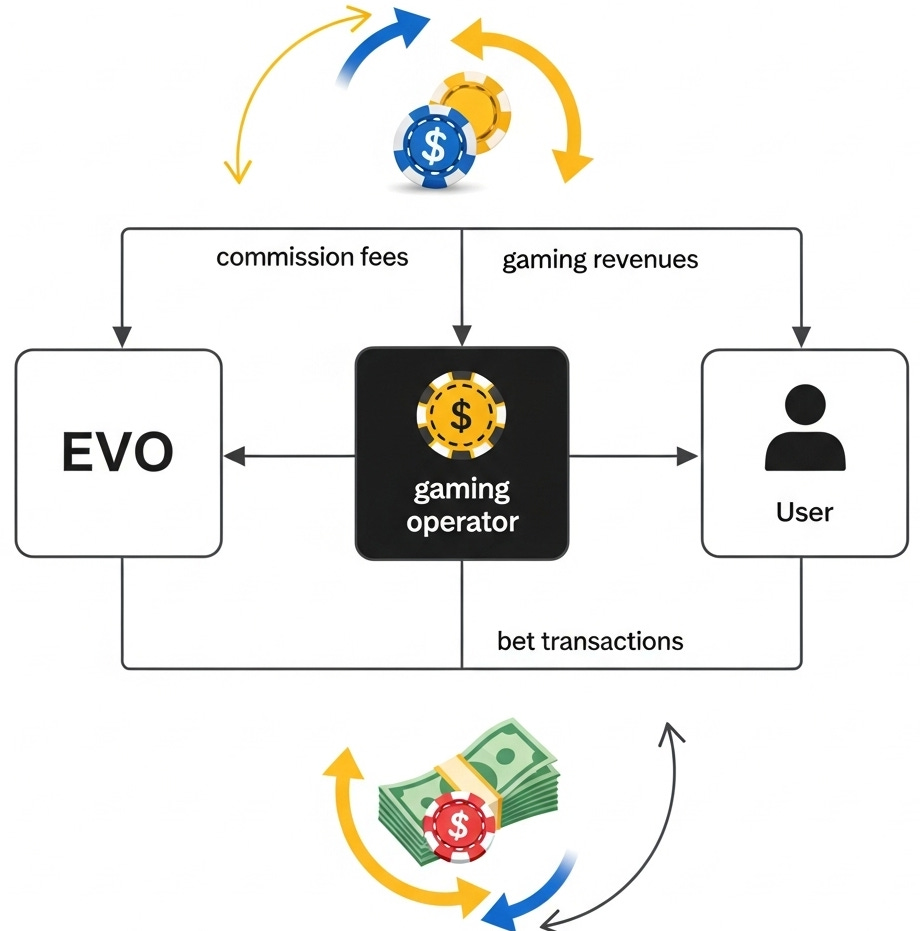

Importantly, Evolution doesn't run casinos. It operates a platform model, supplying operators with high-margin content and infrastructure while avoiding regulatory baggage and customer-facing risk.

Revenue Structure

Commissions (8–15%): The bulk of revenue comes from a fixed percentage of operator winnings generated from Evolution games. This scales automatically as client casinos grow.

Dedicated table fees: Fixed fees charged for exclusive studio tables with branded dealers or custom visuals.

Setup & Integration fees: One-time payments for onboarding new clients.

RNG/Slot games: Added via acquisitions like NetEnt and Red Tiger, giving them a secondary revenue stream and helping them diversify from purely live content.

Evolution operates through its OSS-model (One-Stop-Shop), which allows casino operators to seamlessly integrate the entire game portfolio into their platforms. This setup gives operators easy access to Evolution’s full offering, from live casino games to RNG titles. What makes Evolution stand out is how vertically integrated they are — they don’t just build games, they own the whole experience: from game design and software to hiring and training the live dealers. Even the betting infrastructure is handled by them. The only major responsibility left to the operator is regulatory compliance, including KYC (Know Your Customer) and local licensing — Evolution stays out of that legal burden, but provides everything else.

From their own 10K — the OSS-model looks like this:

III. Valuation

P/E Ratio (TTM): ~10.5 — near decade lows, down from 21.9 in 2023.

Market Cap: $13.7B USD — down over 40% YoY…?

Debt-to-Equity: 0.01 — basically no debt which is very, very good.

Free Cash Flow Margin: 63% — almost flawless.

Gross Margin: ~90%

Operating Margin: ~63%

Net Profit Margin: ~55%

Revenue (TTM): $2.24B — up from $1.95B in 2023.

Dividend Yield: 4.91% — and it keeps growing…

Current Stockprice…

Year-to-date, Evolution is down over 42%. So what gives? The fundamentals are nearly flawless. The margins are out of this world. The business model prints cash. So why the sell-off?

Well — first of all, it's a sin stock. That means sentiment is biased against it from the start. People don’t want to like gambling companies. It feels dirty. Investors tell themselves they’d never profit off someone else’s misery. Ironic, considering Evolution doesn’t even run the casinos — they provide the infrastructure. The dealers, the tech, the real-time games. They're a supplier, not the house. But it doesn’t matter. The ESG crowd clutches pearls anyway.

This sentiment problem means the bar is set stupidly high. When Q1 2025 earnings dropped and missed analyst expectations on growth — despite posting a 16% YoY revenue increase and over 55% profit margins — the market didn’t flinch… it panicked. The stock got hammered down to levels we haven’t seen since 2020. All because “just growing profitably” isn’t good enough when you’re Evolution.

But sentiment isn’t the only thing weighing down on Evolution.

Regulatory heat is somewhat real — even if it’s mostly just fog... The EU has been considering tighter restrictions on online gambling, and while no major hammer has dropped, the fear alone is enough to scare off soft hands. Evolution also operates in fragmented legal landscapes (think: Sweden, UK, Malta, Curacao), and every time some local regulator sneezes, investors fear a literal pneumonia diagnosis.

Then there’s the Capital Group’s recent selloff — one of the largest shareholders quietly reducing exposure. Retail saw that and assumed something must be wrong. But big players rotate portfolios all the time. Ironically, Kenneth Dart, a billionaire investor with a reputation for betting against the herd and being right about it, increased his position while everyone else panicked.

And yeah, the valuation was perhaps a bit stretched. Let’s be honest — Evolution was priced like a tech unicorn post-COVID during 2021. And now, that it's merely “growing fast with world-beating margins,” some tourists are cashing out. That’s their loss.

IV. Hidden Gem

Despite the sell-off, few companies on the planet have Evolution's blend of moat, margins, and misunderstood narrative.

1. Competition? Practically none.

Nobody does what Evolution does at scale. Not Playtech, not Pragmatic Play(except for blackjack). Their tech moat, studio quality, game variety, and dealer training pipeline puts them DECADES ahead.

In the 10-K for 2024, the CEO himself addressed the elephant in the room: “Barriers to entry are low — but the barriers to success are extremely high.” While technically, anyone can build a live casino game. I can't imagine anyone pulling off Evolution’s scale, trust, and studio quality? That’s a whole different beast! And even if some copycat manages to mimic the visuals… Personally, I’d still much rather play on Evolution’s infrastructure than trust some knockoff outfit from Shenzhen streaming out of a warehouse. Gambling is partly about trust — and Evolution owns that trust.

And let’s be honest: most competitors are chasing, playing catch-up, not innovating. Evolution is already three steps ahead, running Emmy-tier game shows while others are still figuring out how to sync cards with a webcam.

2. Billionaire Kenneth Dart is buying.

While funds like Capital Group trimmed positions (probably rotation), Dart increased his stake. This guy loves money, where he goes → money follows. He’s known for high-conviction bets in unpopular places and often ends up being early and right — from distressed sovereign bonds to tobacco and pharma. His involvement isn’t just noise. It’s signal. When Capital Group sold and Dart picked up that’s blood in the water, and sharks move first.

3. The CEO has grit.

Martin Carlesund is underrated. He doesn’t care much for headlines. What does he do? Executes. Every. Single. Quarter. He led the company from niche player to market dominator and routinely deflects pressure to over-communicate or sugar-coat guidance. This laser focus has kept Evolution lean, profitable, and global — while avoiding bloated marketing or overexpansion pitfalls. In an interview before the all time highs in 2021, he stated regarding competition “it’s about being both hungry and paranoid”. I don’t know about you, but that is the kind of CEO I like.

4. AI...

In an era where artificial intelligence is poised to take over numerous tasks, Evolution's greatest asset resides within its humanity. Even as we move toward a future dominated by artificial intelligence, Evolution's real-time-dealers remain integral to the entertainment experience. While AI can enhance efficiency and perhaps quality, it cannot replicate the thrill of a live host spinning the wheel or interacting with players, celebrating significant wins. This connection I believe ensures their continued relevance in the industry.

Ultimately, while AI may disrupt content creation and streamline trading processes, the enduring appeal of live entertainment, facilitated by human interaction, will prevail in the long run. Additionally the game creation Evolution provides isn't just quantity but also quality which further solidifies them over the long run.

Why Evolution is a Hidden Gem?

Evolution isn’t just another growth stock. It’s a cash-flowing monopoly disguised as a casino supplier. Beneath the charts and quarterly updates, what you're really buying is:

— An underappreciated misunderstood OSS-like business model, where one studio can scale infinitely across the globe at near-zero marginal cost.

— An IP moat that transforms gambling into immersive entertainment.

— A culture that’s hungry, paranoid, and relentlessly execution-focused.

— Defensibility even in the age of AGI, thanks to the irreplaceable role of live human interaction.

AND EVEN IF IT FLOPS AND DOESN'T RECOVER YOU STILL GET GREAT DIVIDENDS!

V. Why I am buying

So, after all the noise, the market freak-outs, and the ESG pearl-clutching, why am I putting my capital into Evolution Gaming? Because this isn't just another stock. This is almost a once in a lifetime opportunity as this rare convergence of a world-beating business model, untouchable competitive advantages, and a valuation that defies logic. It isn't just a market leader — it is the market! They own 70% of the market share and they currently penetrating into Asia with ongoing cyberattacks...

What you're buying here isn't a flash-in-the-pan growth story, but a cash-printing machine with a strategic depth almost no companies can realistically match. I bought Evolution at $90 a share — even then it was massively undervalued — and I have kept buying ever since. Furthermore I am going to keep buying when it trades down as well as keep buying all the way up.

You are getting a business with 60-70% EBITDA margins, over 50% FCF magins and not to mention double-digit return on investment with a P/E of 10... AND THEY ARE BUYING BACK SHARES!

I predict this stock is going to recover, slowly but surely, they just intitated share buybacks yet the stock price is deadlocked between $60-70... In a year or so i expect the market to catch up and it will reach new highs.

But this isn't about next year, 38% of my holdings consists Evolution, this is about where it will be 2027 or later, I see a huge opportunity. Those who didn't buy today will look back in regret, that won't be me.

I'm not buying Evolution Gaming as quick trade — I am buying because it’s one of the most profitable, vertically integrated business with an unparalleled competitive moat, trading at an absurdly low valuation due to irrational market sentiment.

This isn't a gamble; it's a conviction bet on a fundamentally superior company that the market is currently, and foolishly, sleeping on. It is only a matter of time before the market reprices it. And even if the recovery takes time, those incredible dividends offer a compelling return while we wait for the rest of the world to wake up. Evolution is misunderstood, mispriced, and built for the long game. While others chase hype, I'm buying substance — with dividends. Let them sell. I'm staying at the table.

Disclaimer: This post is for informational and entertainment purposes only. It reflects personal opinions and is not intended as financial advice. Always do your own research before making investment decisions.

Great post on evolution. I really like your writing style and especially the Yu-Gi-Oh! reference at the end :)

Hey Christian it’s Steve from Healthspan Discord Server