Evolution AB: Unjustified Discount on a Global Monopoly?

The cost of perpetual controversy and maybe it’s a gift to smart & patient investors?

Evolution AB:

Valuation vs. Virtue

End of Drama?

Evolution Gaming ($EVO) the live casino titan that trades as if it’s about to be delisted. It attracts worse publicity than most conglomerates, constantly associated with the filth being gambling. A fate not shared by the other B2B suppliers. This is personal since I bought in at €110, I look dumb → and I can’t stand it. Between the relentless ESG virtue signaling and the constant stream of bad headlines, one has to ask: what is truly driving this valuation collapse? Let’s try to dumb this down…

The list of recent controversies is long and varied:

Market Noise: Last year’s Capital Group sell-off, the dramatic Georgian studio strike, ongoing cyberattacks from Asia and leaked reports of fraudulent black-market activity in Africa.

Nominal Q2 revenue growth was modest: (3.1%), but at constant currency, it was 8.8%. (meaning the market is incorrectly pricing in a secular decline when the reality is a temporary regulatory headwind).

Regulatory Fear: Concerns about new EU restrictions on gambling (which never emerged?) and lingering legal disputes hindering U.S expansion.

Nothing groundbreaking in my opinion. Word on the street is that EVO’s glory days are behind them, I disagree. While sentiment remains overwhelmingly negative. Key insiders are showing a different story, one with unparalleled conviction?

CEO Martin Carlesund recently made a significant purchase worth €6.9 million in June 2025. Not particularly bearish here...

Kenneth Dart a mega contrarian investor, has aggressively increased his holding to control almost 20% of the company. This is major conviction which should not be ignored?

A robust share buyback program is underway. (Repurchase of up to €500 million of own shares before the next AGM)

The market treats Evolution as if its stock momentum is broken, but this view is fundamentally flawed. I will prove it ; while the hyper-growth of the initial live casino surge won’t rematerialize, the market is entirely missing the two unpriced growth drivers which I believe will redefine the next decade.

The Unpriced Global Moat

The genius of Evolution is more than the creation of live casino gaming, that part is now well-established. The new obstacle harboring the ultimate opportunity, is the fact that gaming is still an emerging market worldwide, with black markets remaining off-limits to this legal enterprise.

This is where Evolution’s true deep MOAT is found and entirely unpriced by the market at this moment:

Global Compliance Infrastructure: Evolution Gaming has a proven, almost global track record of building complex compliance systems to meet the differing and strict laws across Europe, Asia and North/South America. No competitor is expanding this enterprise-level compliance infrastructure at this scale.

The US Regulatory Surge: Evolution just recently completed its entry into all seven US states currently offering regulated online casino gaming, including a new partnership in Rhode Island. If they can solidify its presence it will unlock a growth surge unlike any before it. The market is not pricing this crucial expansion and regulation-building success.

Decade-Ahead Innovation

Lastly the market remains oblivious to the sheer genius of its innovation engine. As I touched upon in my previous post: Evolution’s tech stack, studio quality, vast game variety and rigorous dealer pipeline puts them decades ahead of rivals. Competitors are playing catch-up, trying to get a slice of the existing pie while Evolution is constantly innovating and creating the next pie with over 110 new games promised this year alone.

I honestly believe this combination of insider confidence, an unpriced global regulatory MOAT plus the unrelenting innovation means the stock is trading at an unjustified discount.

The New Controversy?

But before trying to evaluate this stock, buckle up there is more to uncover… Recently Evolution actually experienced a major win: although most missed it. Basically what happened was that the US class-action lawsuit accusing the company of securities fraud was permanently dismissed. It was a major potential setback for its expansion into the U.S, I was suprised this didn’t move the stock much to be honest.

Unfortunately nothing ever comes easy with Evolution, a new lawsuit has emerged from California involving one of their subsidaries NetEnt for aiding and abetting illegal gambling within the state. It’s about some patent infringement from Taiwan. Probable outcome? Likely minimal impact. But the history shows us that not all publicity is good publicity for EVO…

The first major legal risk is gone, and the second I’d say is contained. For a company with this scale of innovation and regulatory infrastructure it’s just a typical day at the office. Point is that these headlines will likely keep the stock nuked, while more buying opportunities are nice… it’s getting to me tbh.

Valuation

Full transparency here, I’m not the fiercest financial analyst the world has ever seen(yet), but I figured I would just look at some simple data points and draw my own conclusions from them.

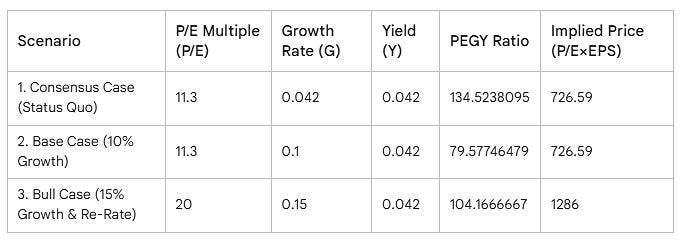

Nightmare chart for real, but I will overlook the technical analysis and leave that to my dad. Regarding today’s valuation I will consult the PEGY-ratio: Peter Lynch-style. You take the P/E and divide it by (growth + dividend yield). Simple enough.

P/E = 11.3,

Growth ≈ 4.4%,

Dividend = 4.2%

PEGY = 11.3 ÷ (4.4 + 4.2) = 1.33 (> 1.0 is Overvalued)

BUT HOLD ON! The market is pricing EVO like it’s dead. A P/E of 11.3, growth ~4.4%, dividend 4.2% = PEGY 1.33!!!

Overvalued? NO!

Mispriced? Absolutely.

The market isn’t expecting any growth at all and thus attributing a very conservative multiple. In another scenario with just a slight uptick in sentiment it could look completely different.

The Current Status Quo

The current price of 726 SEK is only justified if you believe Evolution, a cash-rich, debt-free global leader, will manage a minimal 4.4% EPS growth rate. This scenario results in an “overvalued” PEGY of 1.34x, a direct reflection of the market’s unfounded zombie-like growth fears.The Base Case but a Flip…

Assuming a modest rebound to 10% EPS growth instantly makes the stock an undervalued PEGY bargain at 0.80x. At the current 11.3x P/E, the price is simply too low for this level of quality and growth potential in my opinion. Even a return to EPS growth (6–8%) would justify a fair P/E closer to 15x, implying 30–40% upside from today’s levels…

The Bull Case

My conviction scenario of 15% growth, driven by the US surge and the regulatory MOAT, justifies a P/E multiple and a re-rating to 20x. This means the stock’s fair value is 1,286 SEK, representing an approximate 77% upside from the current valuation.

Now, I could be completely wrong, but given everything I talked about from the regulatory MOAT, insider conviction and dismissal of the securities suit… I believe Evolution is finally set up for a major growth re-acceleration. But even with no growth Evolution’s balance sheet (zero debt and 70%+ gross margins) gives it absurd optionality.

My Move?

My portfolio still sits around 25% Evolution.

Down a lot since my last post, but only because other positions have gained.

I haven’t sold a single share, just slowed down my buying.

It’s been rough watching the entire YouTube crowd chase the same tickers: AMD 0.00%↑ , SOFI 0.00%↑ rinse and repeat — while Evolution posts flawless numbers and no one seems to care. The silence around this stock feels almost deliberate.

Worst of all the Youtube crowd will probably be right at the end of the day. I also fear Evolution getting acquired and the potential multibagger gains slipping away like sand running through my fingers…

I’m not going to pretend I’ve nailed this one. My entry in late spring 2024 hasn’t exactly been glorious. But that’s fine Evolution isn’t a trade, it’s a long-term investment.

And I think that’s the Kenneth Dart move: something reliable which the market’s mispricing because it’s too focused on the next shiny AI datacenter.

So I’m staying put. No panic-selling (until we hit the 3,500 SEK mark) and I’m not joining the youtube crowd at least not yet.

Even if Q3 disappoints, I’ll keep buying.

Because deep down, this still feels like one of those rare cases where the market is wrong and not me. (I’m never wrong)

🛰 Signal LOST: End of transmission — INVADER out… 🚀

Disclaimer: This post is for informational and entertainment purposes only. It reflects personal opinions and is not intended as financial advice. Always do your own research before making investment decisions.

Sounds good! I've been looking hard at this one. GuruFocus gives it an 89 out of 100, but they give it a value score of 2/10 which implies it could be a value trap. Value investing says Evolution's fair value is SEK 1525.67! Anyway, I think I'll grab a position as soon as I can shake loose some cash.

Has your thesis changed after reading the Q3 results?